A bad faith insurance claim in California is worth more than the original policy benefits owed. California law stacks four damages categories: contract damages, extracontractual damages, Brandt fees, and punitive damages. Recoveries range from low five-figures on small denied claims to seven or eight figures when punitive damages are included.

Hillguard Injury Lawyers have years of experience pursuing California bad faith disputes against major insurance carriers. Our practice areas cover the auto, homeowner, disability, and health claims most often delayed or denied in bad faith. Schedule a free consultation with us today to put a real number on the recovery.

This blog breaks down each damages category, the factors that push claim value up or down, the punitive damages standard, and common valuation mistakes.

What Determines the Value of a California Bad Faith Insurance Claim

Three drivers move the number: original insurance benefits the carrier wrongfully withheld, financial and emotional fallout of the delay or denial, and severity of the insurance company’s conduct. California law allows a policyholder to recover beyond the original policy limits because insurers are liable for all damages that naturally flow from the misconduct. The table maps the five damage categories.

| Damages Category | What It Covers | Governing Authority |

|---|---|---|

| Contract damages | Policy benefits wrongfully withheld + prejudgment interest | Breach of the insurance contract |

| Extracontractual (tort) damages | Emotional distress damages + consequential economic loss beyond the insurance policy | Egan v. Mutual of Omaha (1979) |

| Brandt fees | Attorney fees incurred to recover policy benefits, recoverable as damages | Brandt v. Superior Court, 37 Cal.3d 813 (1985) |

| Punitive damages | Punishment + deterrence where the insurer acted with malice, oppression, or fraud | California Civil Code §3294 (clear-and-convincing standard) |

| Statutory penalties | $5,000 per Unfair Insurance Practices Act violation; $10,000 if willful | California Insurance Code §790.035 (California Department of Insurance) |

Every figure builds off the contract anchor: the bigger the underlying claim, the bigger the tort, Brandt, and punitive ceilings on top.

Contract Damages: The Floor of Any Bad Faith Case

Contract damages anchor the case; every other bucket scales off them. They equal the full unpaid policy benefits (the initial amount the insurer wrongfully withheld) plus 10% prejudgment interest under California Civil Code §3289(b). On a denied auto-BI, UM/UIM, homeowner, disability, or life loss, that is the same figure the insurance company failed to pay when the file supported coverage. The contract claim closes the gap between what the carrier paid and what the policy owed on legitimate claims.

The valuation of the underlying claim drives the anchor. Adjusters who never read the medical records, asked for the same documents twice, or skipped the policy terms leave the carrier exposed once the court has to make the insurer handle the claim fairly; the insurer’s conduct on the file is where the case lives. Prejudgment interest at a rate of 10% accumulates rapidly. For instance, if there is an unreasonable denial lasting two years on a $100,000 policy limit, it can result in approximately $20,000 in interest alone. Additionally, extended periods of denial can lead to interest increases of 20-40% beyond the original contract amount.

Extracontractual (Tort) Damages: Emotional Distress and Consequential Economic Loss

Tort damages are where the recovery moves past the policy. California treats the implied covenant as a tort duty, so emotional distress damages are recoverable, acknowledging the genuine emotional harm and emotional stress caused by the wrongful denial of an insurance claim, with no statutory cap.

Consequential economic damages cover every downstream loss the insurer’s denial caused: mounting medical bills, missed mortgage payments, damaged credit, foreclosure exposure, lost wages from delayed medical care, having to borrow money against retirement, and the documented financial hardship and financial pressure of running a household on credit. None of these damages is capped; the insurer violates its legal duty to deal fairly and pays for the harm that naturally flows. Tort damages scale with the harm and severity of the denial, the duration of the insurer’s bad-faith conduct, and documented harm and commonly land at 1-3x the contract anchor in severe-conduct files.

Brandt Fees: How Attorney Fees Become Recoverable Damages

Under Brandt v. Superior Court, 37 Cal.3d 813 (1985), attorney fees a policyholder incurs to compel payment of policy benefits are recoverable as damages. Brandt fees equal the share of the contingency fee attributable to recovering the policy benefits, allocated by a jury or trial court. On a $200,000 contract-damages recovery handled on a 40% contingency fee basis, Brandt fees add about $80,000 before calculating tort or punitive damages, with court costs running in parallel. Brandt turns attorney fees from a cost the policyholder absorbs into a damages line the carrier writes a check for, and every month of delay tactics grows the fee allocation.

Punitive Damages: Civil Code §3294 and the Due-Process Ratio Limits

California Civil Code §3294 allows punitive damages on clear-and-convincing evidence of malice, oppression, or fraud. Malice includes conscious disregard of the policyholder’s rights, the standard most first-party files meet when adjuster notes show the carrier knew the claim was payable and stalled anyway. The statute imposes no cap, and the express §3294 rationale is to deter future misconduct.

State Farm Mut. Auto. Ins. Co. v. Campbell, 538 U.S. 408 (2003), caps the punitive-to-compensatory ratio on due-process grounds: above 9:1 is presumptively unconstitutional, and 4:1 or lower is most defensible. BMW of North America v. Gore, 517 U.S. 559 (1996), adds three guideposts: degree of reprehensibility of the insurer’s misconduct, ratio to actual harm, and comparable civil or criminal penalties. Repeated denials, “pad the file” memos, and pattern conduct push the ceiling higher. On a $300,000 compensatory total, a 4:1 ratio yields nearly $1.2 million, while a 9:1 ratio approaches $2.7 million.

“Section 3294 has no statutory cap, and that headline misleads policyholders. The constitutional ratio rule limits it. Above roughly a single-digit ratio to compensation, the award gets reviewed on due-process grounds and often comes back down. Punitive exposure is real, but the practical ceiling is set by Campbell and Gore, not by statute,” said David E. Jacobson, managing partner at Hillguard Injury Lawyers.

Statutory Penalty Exposure: Insurance Code §790.03 and §790.035

Bad faith insurance practices trigger a separate administrative penalty stacked on top of civil damages. California Insurance Code §790.03(h) lists prohibited unfair insurance practices: unreasonable delays, failure to acknowledge communications about a claim promptly, failure to run a complete investigation or properly investigate the loss, requesting the same documents multiple times, misrepresenting policy terms, and lowball settlements on documented valid claims. Section 790.035 sets the math: $5,000 per Unfair Insurance Practices Act violation, $10,000 if willful, assessed by the California Department of Insurance; 100 willful violations equal $1,000,000 separate from civil damages.

Under 10 CCR §2695.5(b) and §2695.7(b), the insurer must acknowledge communications about a claim within 15 days and decide coverage within 40 days of proof of loss. Missing those deadlines is one of the clearest patterns of bad faith insurance practices the regulations recognize. Common conduct triggers include denials with no clear legitimate reason, lowball offers below the documented value of valid claims, and asking for the same medical records twice, each serving as key evidence in the claim file.

Not all insurance companies act on the math the same way; some settle once the violation count climbs, and others gamble that the policyholder runs out of time. The CDI’s May 2026 Accusation against State Farm, which is a formal administrative action and not a verdict, is a current example of statutory math running parallel to civil exposure when insurance companies act outside the regulations.

Factors That Drive Bad Faith Claim Value Up

The same contract anchor produces a very different bad faith claim, depending on what the carrier did and how. The table maps the six factors that most often push the number higher.

| Factor | Impact | Why It Matters |

|---|---|---|

| Severity of denial conduct | Pushes tort + punitive damages higher | A flat, unreasonable denial reads differently than a documented coverage dispute |

| Evidence of malice or fraud (conscious disregard) | Triggers §3294 punitive damages | Adjuster notes and “pad the file” memos are the key evidence |

| High policy benefits / large underlying claim | Bigger contract base → every stack scales | Tort, Brandt, and punitive damages all calculate off the contract anchor |

| Pattern of similar bad faith insurance practices | Raises reprehensibility under BMW v. Gore | Prior CDI findings and similar suits show a pattern |

| Vulnerable policyholder | Raises reprehensibility | Courts treat conduct against elderly, disabled, or bereaved claimants more harshly |

| Long duration of tort and bad faith | Raises tort + Brandt fees | Every month of delay tactics compounds emotional distress, damages, lost wages, mounting medical bills, and attorney fees |

Factors That Drive Bad Faith Claim Value Down

Four discount factors pull the number down.

The genuine dispute defense under Wilson v. 21st Century Ins. Co. is the strongest one. A carrier can point to a real coverage dispute when reasonable standards evaluate it. The valuation of the underlying claim drives the anchor. The defense is narrow, but it is still available.

Policyholder credibility issues make it harder for the carrier to maintain its position. Inconsistent statements, late notice, prior insurance fraud allegations, and social-media evidence contradicting damages all weaken the file.

Comparative fault or coverage issues on the underlying claim shrink the contract anchor. UM/UIM disputes with contested liability, homeowner claims with arguable exclusions in the insurance policy, and disability files with pre-existing condition disputes reduce the base from which every stack is calculated. Carriers pursuing their own interests press exclusions hard.

Recoverability caps also matter. Uncollectible defendants and individual-versus-corporate carrier wealth limits change what a verdict actually collects.

Why a Low-Value Underlying Claim Can Produce a High-Value Bad Faith Recovery

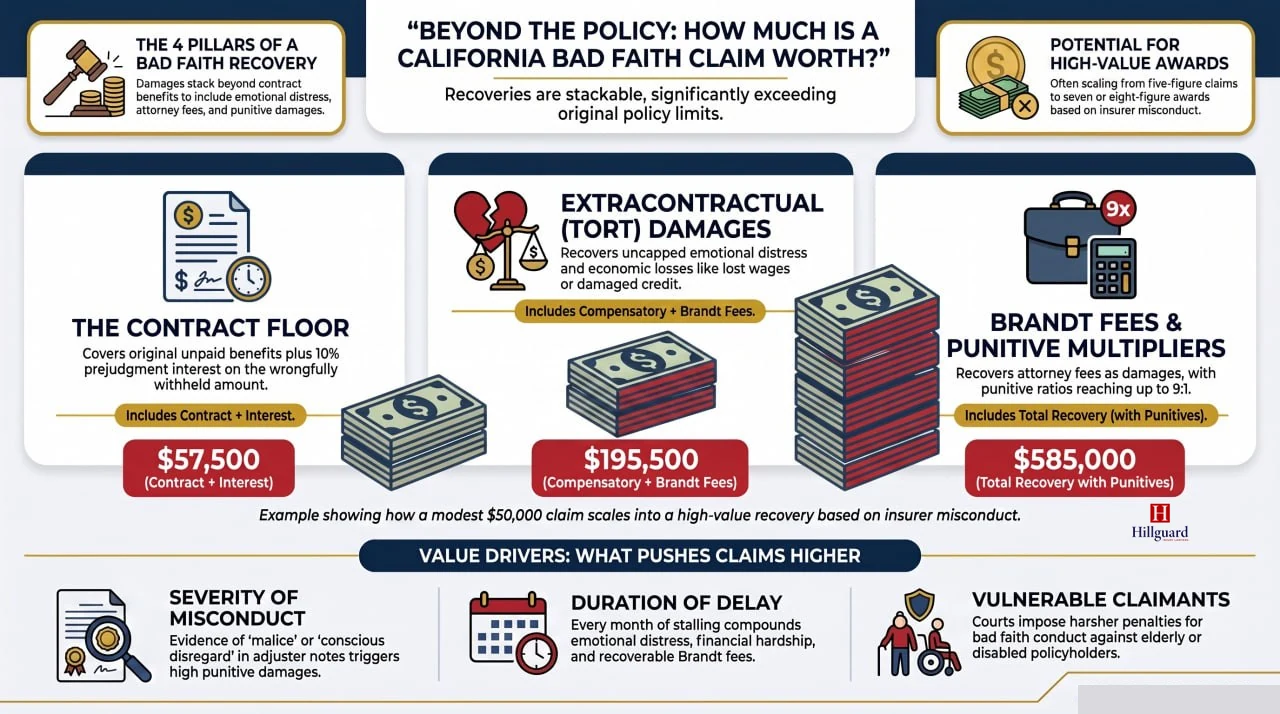

The arithmetic below shows how a modest underlying claim turns into a much larger recovery once the insurer’s misconduct fills in the rest of the stack, the kind of file California car accident attorneys see regularly. Assume a $50,000 covered auto-BI or UM/UIM loss, an 18-month unreasonable denial, adjuster notes ignoring the medical records and policy terms, and a policyholder facing mounting medical bills, lost wages, financial hardship, and documented financial pressure after having to borrow money against retirement.

- Contract damages: $50,000 + ~$7,500 prejudgment interest = $57,500

- Extracontractual (tort) damages: emotional distress + lost wages + downstream economic loss at 2x the contract anchor = $115,000

- Compensatory subtotal: ~$172,500

- Brandt fees: 40% × $57,500 = ~$23,000

- Combined compensatory + Brandt: ~$195,500

- Punitive damages: 2:1 ratio under Campbell = ~$390,000

- Total bad faith recovery: ~$585,000 on a $50,000 underlying claim.

Without punitives, the total lands near $195,500; with a 4:1 ratio on stronger malice evidence, it approaches $975,500. The policy benefits limit applies solely to the contract portion; all other damages increase based on the insurer’s actions, and this calculation is central to California insurance bad-faith cases.

Settlement Valuation Considerations: How Insurers Calculate Their Exposure

Carriers run the same math from the other side. Defense fees, expert witnesses, and claim-handling deposition risk add real cost, and verdict exposure that makes the news affects the carrier’s California book of business; sophisticated insurers price reputational risk into the claims process. The administrative exposure under §790.035 operates concurrently, so an insurer undergoing a CDI examination, facing a private lawsuit, and having a documented count of violations must assess its total exposure across all these situations. According to the Judicial Council of California, 83% of unlimited civil cases in CA superior courts were disposed of before trial in FY 2024-25.

Additionally, Brandt fees and punitive exposure are the strongest pressure points; settlements typically clear the compensatory subtotal but discount the punitive ceiling by 30-70% for appellate risk, and most first-party insurance bad faith cases settle within 12-36 months.

Common Mistakes to Avoid When Valuing a California Bad Faith Claim

Valuation mistakes reduce the amount you recover. Each one below weakens the damages stack, hands the carrier leverage, or forfeits a recovery line that California law would otherwise put on the file.

- Don’t settle for unpaid policy benefits alone. Taking the unpaid policy benefits and walking forfeits the tort bucket, Brandt fees, and §3294 punitive exposure. The contract recovery is the floor, not the ceiling.

- Don’t trust the insurer’s valuation of your claim. The carrier’s first offer is a test, not a reserve. Adjusters start with a low offer to test whether you have legal counsel and a detailed damages file prepared.

- Don’t ignore Brandt fees in settlement calculations. Brandt math changes leverage on every file. Settling without allocating the contingency fee on the policy-benefits portion, as doing so may limit your recovery to what is documented at that time, allowing the carrier to benefit from that line without cost.

- Don’t underestimate the punitive damages exposure. The §3294 clear-and-convincing standard sounds steep, but conscious disregard is what most first-party files actually show on the claim notes. Campbell single-digit ratios cap the upper end, but the floor on a documented malice file is meaningful.

- Don’t settle before the damages stack is fully built. Emotional distress documentation, lost wages records, the financial hardship paper trail, Brandt allocation, and adjuster-conduct depositions take time to develop. Settle early, and the recovery caps at whatever the file shows that day.

- Don’t fail to document financial hardship and emotional distress. Consequential economic damages and emotional distress damages are the largest non-statutory drivers, and they live or die on documentation. Bank statements, medical records, retirement-withdrawal records, therapy notes, and a contemporaneous timeline of every communication are the proof.

- Don’t accept policy limits as the recovery cap. The policy face caps the contract piece, nothing else. Tort, Brandt, and punitive damages are not bound by the policy benefits limit.

- Don’t try to value a bad faith case with a general PI lawyer. Bad-faith valuation requires expertise in adjuster-conduct depositions, claim-file analysis, and coverage-expert review; work that a general PI practice does not run on every file. A free consultation with a California bad faith specialist is the right starting point.

“The mistake I see most: the carrier finally pays the policy benefits, the policyholder is relieved, and the file closes. That payment is the contract floor. It does not address tort damages, Brandt fees, or punitive exposure for the conduct that delayed the payment in the first place. Getting paid is not the same as being made whole,” said David E. Jacobson, managing partner at Hillguard Injury Lawyers.

Get a Real Valuation of Your California Bad Faith Claim

Bad faith claims in California are worth far more than the original policy amount when the damages stack is built right. Contract damages, extracontractual damages, Brandt fees, and punitive damages can multiply the recovery, and waiting can shrink it. Calling a bad faith insurance attorney now protects the deadlines, preserves the claim file, and keeps every recovery category on the table.

Hillguard Injury Lawyers represents California policyholders against major insurance carriers in bad faith disputes statewide. An experienced bad-faith insurance lawyer can break down the damages buckets, document the carrier’s conduct, and put a real number on the recovery. Contact us today for a free case review.

Frequently Asked Questions About California Bad Faith Claim Value

Hillguard’s experience handling California insurance bad faith cases shapes the answers below. Each is a starting point; a consultation with an experienced attorney or a qualified attorney at the law firm is the only way to put real numbers on a specific bad faith insurance claim.

What Is the Average Bad Faith Settlement in California?

No published “average” exists; settlements track the facts of each file. Mid-six figures is common on first-party files with a year or more of unreasonable denial; seven- and eight-figure recoveries appear when punitive damages stack on substantial compensatory damages.

Can I Recover Punitive Damages in a California Bad Faith Case?

Yes, where the insurer acted with malice, oppression, or fraud (including conscious disregard) proved by clear-and-convincing evidence under California Civil Code §3294. No dollar cap, but State Farm v. Campbell limits the ratio to single digits in most files.

How Are Brandt Fees Calculated in California?

Brandt fees equal the share of the contingency fee attributable to recovering the policy benefits, allocated by jury or court. On a 40% contingency case with $200,000 contract damages, Brandt fees typically land near $80,000, separate from court costs.

What Is the Maximum Punitive Damages Ratio Allowed in California?

No statutory cap, but State Farm v. Campbell (538 U.S. 408) and BMW v. Gore (517 U.S. 559) limit ratios to single digits on due-process grounds. Above 9:1 is presumptively unconstitutional; 4:1 or lower is most defensible.

How Long Does It Take to Settle a California Bad Faith Insurance Claim?

Most first-party cases settle in 12-36 months; contested malice evidence takes longer. The tort statute of limitations is two years; breach of the written insurance contract is four.

Does the Size of My Underlying Policy Limit My Bad Faith Recovery?

No. Tort damages, Brandt attorney fees, and punitive damages are not capped by the underlying insurance policy face value. The policy benefits limit caps only the contract damages line.

Can I Recover Emotional Distress Damages in a Bad Faith Case?

Yes. California recognizes emotional distress damages as a tort component of a bad faith insurance claim, with no statutory cap. They often equal or exceed the contract damages anchored in severe-conduct files.

Do California Bad Faith Lawyers Work on a Contingency Fee Basis?

Most California bad faith law firms handle first-party files on a contingency fee basis, with no attorney fees up front, court costs advanced, and payment due only on recovery. This guide does not constitute legal advice; confirm the fee structure during a free case review.

Legal Disclaimer

The information on this website is for general informational purposes only and does not constitute legal advice. No attorney-client relationship is formed by use of this site. Past results do not guarantee future outcomes. Every case is unique and must be evaluated on its own facts. If you need legal advice, please contact our office for a free consultation.