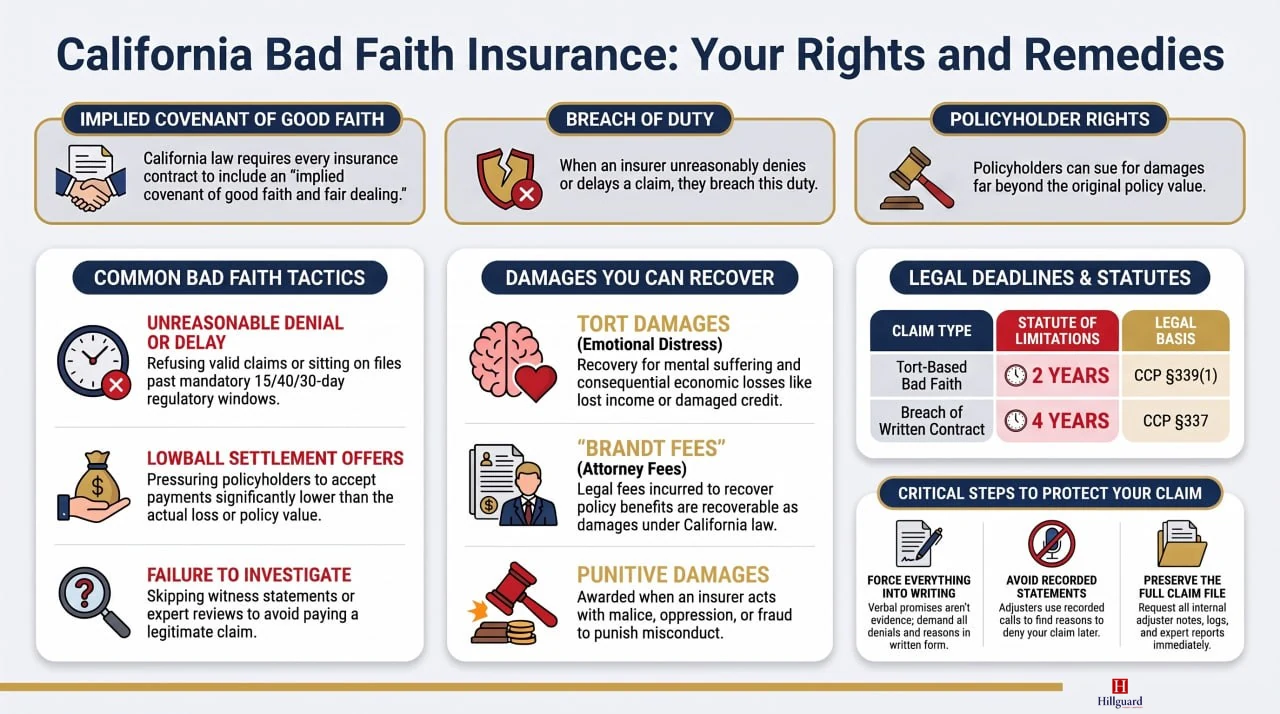

California bad faith insurance law is the body of state common-law and statutory rules that lets a policyholder sue an insurance company for unreasonably denying, delaying, or underpaying a valid insurance claim. The doctrine rests on the implied covenant of good faith and fair dealing built into every insurance contract under California law, which courts treat as both a contract obligation and a separate tort duty. That tort/contract duality is what opens up damages beyond the policy value itself, including emotional distress, attorneys’ fees, and in some cases, punitive damages.

Hillguard Injury Lawyers has years of experience handling California bad faith insurance disputes for policyholders across the state, from auto and homeowner denials to disability insurance and life claims. The work sits alongside our other practice areas in personal injury and employment matters, which gives the team a wide read on how insurance companies behave once a real claim lands on the desk. Contact us for a free consultation if an insurer has denied, delayed, or lowballed a claim you believe is owed.

This article walks through the doctrines that define California bad faith, the damages you can recover, the deadlines that govern your case, and the tactics insurers use to fight back.

What Is Bad Faith Insurance in California?

Insurance bad faith happens when an insurer unreasonably withholds or denies benefits owed under the policy. California law treats that misconduct as both a breach of contract and a separate tort, which lets a policyholder recover damages beyond the policy value. The standard reaches first-party and third-party claims arising under auto, homeowner, disability insurance, health, life, and liability coverage.

Every insurance contract in California carries an implied covenant of good faith and fair dealing, and insurance companies are legally obligated to investigate fairly against reasonable standards and pay valid claims when the file supports payment. Comunale v. Traders & General Ins. Co., 50 Cal.2d 654 (1958), locked that obligation in for liability carriers; Gruenberg v. Aetna Ins. Co., 9 Cal.3d 566 (1973), extended it to first-party claims and tied insurers to an equal-consideration rule: the insurer must give the insured’s interests at least as much weight as its own. When an insurance company breaches that duty, the policyholder gets tort remedies on top of contract relief.

First-party bad faith covers claims an insured files for their own loss, such as a car accident covered by collision or UM/UIM, a homeowner fire, or a disability insurance denial. Third-party bad faith involves liability coverage and the insurer’s duty to defend and settle a suit against the insured. Same implied covenant; different proof and damages math.

“What separates bad faith from a regular breach-of-contract case is that the policyholder gets tort remedies on top of the contract. That is why emotional distress, attorney’s fees, and punitive damages are on the table. California treats the implied covenant as both a contract obligation and a separate tort duty,” said David E. Jacobson, President and Managing Partner at Hillguard Injury Lawyers.

Common Tactics That Constitute Insurance Bad Faith in California

The California Department of Insurance (CDI) has accused State Farm of 432 violations of the Unfair Insurance Practices Act, which include 398 violations identified during a market conduct examination and 34 from consumer complaints. The maximum penalty could reach $2.16 billion, making it the largest case pursued this century following a wildfire disaster.

Most bad-faith cases come down to a small set of recurring tactics. The table pairs each one with what the insurer typically does and why California law may treat it as a basis for bad-faith litigation, providing a pattern-match cheat sheet for unfair claims-settlement practices in real files.

| Conduct | What the Insurer Did | Why It May Constitute Bad Faith Under California Law |

|---|---|---|

| Unreasonable denial of a valid claim | Refuses to pay despite a covered loss | Insurer denies benefits unreasonably when the file shows coverage |

| Unreasonable delay | Sits on the claim past the 15/40/30-day windows | Violates 10 CCR §2695.5(b), §2695.7(b), §2695.7(h) of the Fair Claims Settlement Practices Regulations |

| Lowball settlement offer | Sends a settlement offer well below the actual loss | Pressures claimants to accept far less than the policy benefits owed |

| Failing to investigate | Skips records, witness statements, and expert review | Fails the proper investigation, and the implied covenant requires prompt investigation |

| Failure to defend | Refuses defense counsel on a covered liability claim | Breaches the insurer’s defense obligation under the policy provisions |

| Failure to settle within limits | Rejects a reasonable settlement on a covered claim | Excess judgment exposure under Crisci v. Security Ins. Co. (1967) |

| Misrepresenting policy terms | Tells the insured that a covered loss is excluded | Misstating policy provisions or relevant facts can constitute bad faith |

| Forcing suit on a legitimate claim | Refuses payment, betting the insured will not sue | Forcing policyholders to court to recover legitimate claim amounts is a recognized tactic |

California’s Fair Claims Settlement Practices Regulations under Title 10 of the California Code of Regulations §2695 establish strict timing requirements for every claim denial. Insurers must acknowledge claims within 15 days (10 CCR §2695.5(b)), accept or deny claims within 40 days after proof of loss (10 CCR §2695.7(b)), and pay claims within 30 days after settlement (10 CCR §2695.7(h)).

When an insurance company engages in repeated delays or moves to deny claims without proper cause, such conduct can support a bad-faith claim, and the financial strain and emotional distress on the policyholder become recoverable harm.

The Legal Framework: California Statutes and Case Law

California bad faith insurance law is anchored to a tight set of authorities. Comunale (1958) and Gruenberg (1973) define the implied covenant; Crisci (1967) sets the failure-to-settle rule. Egan v. Mutual of Omaha Ins. Co., 24 Cal.3d 809 (1979), holds that a first-party insurer’s bad faith sounds in tort and supports recovery for emotional distress and consequential economic loss. Brandt v. Superior Court, 37 Cal.3d 813 (1985), makes attorneys’ fees incurred to recover policy benefits recoverable as damages.

Insurance Code §790.03(h), part of the Unfair Insurance Practices Act, lists prohibited insurer behaviors: misrepresenting policy provisions, failing to act on claims with reasonable promptness, and not attempting good faith settlement when liability is reasonably clear. Moradi-Shalal v. Fireman’s Fund Ins. Co., 46 Cal.3d 287 (1988), held that there is no private right of action under §790.03 directly, but the statute still anchors the obligation insurers carry under California law and supplies the regulatory backbone the California Department of Insurance enforces. With 10 CCR §2695, these authorities help determine whether the insurer acted reasonably under the agreement.

How to Prove a California Bad Faith Insurance Claim

To prove a bad-faith claim, the policyholder must establish two elements from Wilson v. 21st Century Ins. Co., 42 Cal.4th 713 (2007): benefits due under the insurance policy were withheld, and the withholding was unreasonable or without proper cause. Both turn on the circumstances of the file. Element one is coverage, an enforceable insurance contract in force at the time of loss and a loss the policy covers, read against the policy terms and exclusions. Element two is where most cases live: the court will determine whether the carrier’s conduct fell outside what a reasonable insurer would do on the same facts. Missing the 10 CCR §2695 timing rules, ignoring favorable expert evidence, and inventing reasons not in the policy provisions all point toward unreasonable behavior.

The claim file, which contains adjuster notes, logs of claim handling, recorded statements, denial letters, and expert evaluations, serves as the central evidence in the case.

Damages Available in a California Bad Faith Lawsuit

A successful bad-faith claim opens up a full array of remedies that a straight breach-of-contract suit does not. The available compensation falls into four categories: contract, tort, attorneys’ fees as damages, and punitive damages, plus prejudgment interest. The table breaks down what each category covers and the legal authority behind it.

| Damage Category | Legal Basis | What It Covers |

|---|---|---|

| Contract damages | Breach of the insurance contract | Full value of policy benefits wrongfully withheld, plus interest |

| Tort damages (Egan) | Tort cause of action for breach of the implied covenant | Emotional distress and consequential economic damages beyond the policy |

| Brandt fees | Brandt v. Superior Court, 37 Cal.3d 813 (1985) | Attorneys’ fees incurred to recover policy benefits, as damages |

| Punitive damages | Civil Code §3294 | Clear and convincing evidence of malice, oppression, or fraud |

Contract damages cover the full amount of the original claim wrongfully withheld plus prejudgment interest. Tort damages, rooted in Egan, let the insured recover emotional distress and consequential economic damages, including lost income, missed mortgage payments, and damaged credit, caused by the insurer’s bad-faith conduct, and an unreasonable denial exposes the insurer to tort remedies not available in a standard breach-of-contract case.

Under Brandt, attorneys’ fees the policyholder incurs to recover policy benefits are themselves recoverable as damages, not just costs. Punitive damages may be awarded if the insurer acted with malice, oppression, or fraud. Civil Code §3294 requires clear and convincing evidence, a higher proof standard that allows juries to punish carriers that stiff policyholders to pad premiums and profits.

The Genuine Dispute Doctrine and Other Insurer Defenses

Recognized in Wilson v. 21st Century Ins. Co., the genuine dispute doctrine gives carriers a defense when the insurer’s coverage position was reasonable under the circumstances. If the insurer can point to a real factual or legal dispute it evaluated against reasonable standards, the failure to pay may not rise to bad-faith conduct. Carriers also lean on reasonable reliance on expert opinions, policy exclusions and coverage limits read against the policy terms, and accusations that the insured failed to cooperate or gave late notice. None are automatic; the question is whether the file supports the carrier’s position.

California Statute of Limitations for Bad Faith Insurance Claims

The deadline to sue depends on how the claim is pleaded. Tort-framed bad-faith claims arising under the implied covenant generally fall under a two-year statute, Code of Civil Procedure §339(1), though some authorities apply CCP §335.1; this is fact-specific. Breach of a written insurance contract gets four years under CCP §337. The clock starts when the breach becomes apparent, often the date of denial or final lowball offer, but the discovery rule can shift accrual.

Steps to Take If You Suspect Your Insurance Company Acted in Bad Faith

A bad-faith case is built on what happens in the first few weeks after the denial or delay, not what happens in court two years later. The carrier is already building its file the moment it pushes back on a valid claim, and the policyholder needs to be building one too. Hillguard Injury Lawyers recommends a six-step framework that preserves leverage, protects the statute of limitations, and creates the paper record a court needs to evaluate the insurer’s conduct under the implied covenant of good faith and fair dealing.

Step 1: Document Every Communication on Day One

Open a single file, paper or digital, and log every call, email, letter, name, and date the moment the dispute starts. Note who said what and when. Save voicemails. The case rises and falls on the written record, and the record starts the day the carrier first hesitates.

Step 2: Force Every Denial, Reservation, and Delay Into Writing

A verbal “we’re still reviewing” call is not evidence. Send a written request asking the insurer to put its position in writing, citing 10 CCR §2695.7, which requires the carrier to respond within 40 days of receiving the proof of claim. If the response is silence, that silence becomes part of the record too.

Step 3: Preserve the Claim File and the Full Policy

Request a complete copy of the claim file in writing, including adjuster notes, internal correspondence, and any expert reports the carrier relied on. Save the declarations page, the policy booklet, and every endorsement. If a court later evaluates the insurer’s conduct, the file is the case.

Step 4: Calendar Both Statutes of Limitations

Two clocks run at once. Tort-framed bad faith generally runs two years under CCP §339(1), and breach of a written insurance contract runs four years under CCP §337. Calendar both deadlines for the same day the carrier denies, delays, or lowballs, and assume the shorter one controls until an attorney advises otherwise.

Step 5: File a Complaint With the California Department of Insurance

Consumers can complain directly to the CDI through the consumer portal, and these complaints often prompt the carrier to revisit a denial, especially after the May 2026 enforcement actions that put California insurers on notice. The CDI complaint is not a substitute for litigation. It is a parallel pressure tool.

Step 6: Consult a California Bad Faith Insurance Attorney Before the Deadline Runs Out

First-party bad faith is its own practice. A consultation is free, the statute of limitations is unforgiving, and waiting another month to call rarely helps the file. Hillguard reviews bad-faith disputes at no cost.

When to Contact a California Bad Faith Insurance Lawyer

A bad-faith case turns on facts a policyholder rarely sees, including adjuster notes, internal valuation memos, and claim-handling logs. A lawyer pulls the file in discovery, books the claim-handling deposition, and brings in coverage experts to read the policy provisions against what the insurer actually did. Signs the case needs counsel now: the denial does not match the policy terms, the carrier missed 10 CCR §2695 windows, the settlement offer is a fraction of the loss, or the statute of limitations is closing in.

Common Mistakes to Avoid in a California Bad Faith Insurance Claim

Most bad-faith files lose value before a lawyer ever sees them. Each mistake below either hands the insurer a defense it didn’t have or weakens the proof Wilson v. 21st Century requires.

- Don’t give a recorded statement before talking to an attorney. An adjuster’s recorded call is built for cross-examination. A casual line like “I’m feeling better” or “I’m not sure how it happened” will resurface in a denial letter and at deposition. Tell the adjuster you’ll respond in writing once you have counsel.

- Don’t sign a release or “full and final” document without legal review. A release usually waives every claim tied to the loss, including the bad-faith conduct itself. Once it’s signed, Brandt fees and tort damages go with it. Send the document to a California bad-faith attorney before signing; review is free.

- Don’t post about the claim, the incident, or the carrier on social media. Insurers run social monitoring on disputed files. A vacation photo, a gym check-in, or an angry post about the adjuster will turn up in discovery and will be used to argue that you exaggerated the loss. Lock the accounts and stop posting anything tied to the claim.

- Don’t accept the first lowball offer as the “final” number. The opening offer is rarely the carrier’s reserve; it’s a test. Accepting it ends the claim and gives up tort damages, emotional distress recovery, and Brandt fees. Respond in writing and price the loss against the policy benefits actually owed.

- Don’t miss the statute of limitations. The statute of limitations section above sets the windows: tort-framed bad faith runs two years, breach of a written insurance contract runs four. A missed deadline ends the case, no matter how clean the file. Calendar both clocks the day the carrier denies, delays, or lowballs.

- Don’t let demands, delays, and denials stay verbal. A phone call the adjuster doesn’t return is not on the record. Every payment demand, every request for the claim file, and every response to a denial goes in writing. The paper trail is what proves unreasonable conduct under the implied covenant.

- Don’t hire a general personal injury lawyer for a bad-faith dispute. First-party bad faith is its own practice. Claim-file discovery, claim-handling depositions, expert review of adjuster conduct, and the Brandt fee pleading all sit outside a standard PI workup. Ask whether the attorney has handled first-party bad faith specifically.

- Don’t skip the CDI complaint as a parallel pressure tool. A complaint to the California Department of Insurance under the Fair Claims Settlement Practices Regulations (10 CCR §2695) is not a substitute for a lawsuit, but it can prompt the carrier to revisit a denial. File it in parallel with retaining counsel, not instead of it.

Get Help From a California Bad Faith Insurance Attorney

If an insurance company has denied, delayed, lowballed, or refused to defend a claim you believe is owed, California law gives you a path to recover both the policy benefits and the harm the carrier’s bad-faith conduct caused. Acting early protects the file, the deadlines, and the room to push for full value. Hillguard Injury Lawyers represents policyholders statewide and handles disputes for insureds who have been pushed around by their carriers.

The firm pairs years of experience handling California insurance disputes with a focused, direct approach. Talk to an experienced California bad faith insurance attorney about your claim and bring the denial letter, the policy, and any correspondence from the insurer. Contact us today for a free consultation.

Frequently Asked Questions

Hillguard’s years of experience handling California bad faith insurance disputes shape the answers below. Each question reflects what policyholders ask most often once they suspect their insurer is acting unreasonably.

What Is Bad Faith Insurance in California?

Insurance bad faith in California is an insurer’s unreasonable refusal to pay benefits owed under the policy. Because it breaches the implied covenant of good faith and fair dealing in every insurance contract under California law and counts as both a breach of contract and a tort, the policyholder can pursue extracontractual and punitive damages on top of unpaid benefits.

Can I Sue My Own Insurance Company in California?

Yes. California recognizes first-party bad faith under Gruenberg v. Aetna (1973), which lets a policyholder sue their own insurer for unreasonably withholding policy benefits and recover unpaid benefits plus tort damages for emotional distress, economic loss, attorneys’ fees, and in some cases punitive damages.

How Long Do I Have to File a Bad Faith Insurance Lawsuit in California?

The deadline depends on how the claim is framed. Tort-based bad faith generally carries a two-year limit under CCP §339(1); breach of a written insurance contract gets four years under CCP §337. The exact deadline is case-specific, so confirm with counsel.

Can I Recover Punitive Damages in a California Bad Faith Case?

Yes, when the insurer acted with malice, oppression, or fraud. Civil Code §3294 requires clear and convincing evidence, and the clear and convincing evidence threshold lets juries punish carriers and deter similar conduct in claims arising against other insureds.

What Is the Genuine Dispute Doctrine in California?

Recognized in Wilson v. 21st Century Ins. Co., the genuine dispute doctrine gives the insurer a defense when its coverage position was reasonable under the circumstances. If the carrier evaluated the file in good faith and the dispute was genuine, the conduct may not constitute bad faith.

Do I Have to File a CDI Complaint Before Suing?

No. A complaint to the California Department of Insurance is not a legal prerequisite. It can still be useful—complaints sometimes prompt the carrier to reopen the file—but the right to sue does not depend on it.

Can I Recover Attorneys’ Fees in a California Bad Faith Case?

Yes, under Brandt v. Superior Court, 37 Cal.3d 813 (1985). Attorneys’ fees the policyholder incurs to recover policy benefits are themselves recoverable as damages, not just costs.

Do I Need a Lawyer to File a Bad Faith Insurance Claim?

Strongly recommended. Claim-file discovery, expert review of claim-handling conduct, and the statute of limitations are hard to manage without counsel, and the pleading has to protect tort remedies, attorneys’ fees, and punitive damages.

Legal Disclaimer

The information on this website is for general informational purposes only and does not constitute legal advice. No attorney-client relationship is formed by use of this site. Past results do not guarantee future outcomes. Every case is unique and must be evaluated on its own facts. If you need legal advice, please contact our office for a free consultation.